Table of Contents

- Understanding Tax Structuring

- Choosing the Right Business Entity

- Leveraging Tax Credits and Deductions

- Implementing Proactive Tax Planning

- Staying Compliant with Tax Regulations

- Adapting to Technological Changes

- Considering International Tax Implications

- Conclusion

Starting a new business is an exciting venture, but navigating the complexities of tax laws can be daunting. Implementing smart tax structuring from the outset can significantly influence a company’s financial health and long-term success. Engaging with a knowledgeable business lawyer is crucial in this process. Freeman Lovell, a reputable firm specializing in business formation and tax structuring, offers comprehensive services to help entrepreneurs navigate complex tax landscapes and establish solid foundations for their ventures.

Understanding Tax Structuring

Tax structuring involves organizing a business’s financial and operational framework to optimize tax liabilities. This includes selecting the appropriate business entity, managing deductions, and planning for future tax obligations.

Smart tax structuring is not solely about reducing taxes; it is about establishing strategies that enable businesses to operate more efficiently and effectively. For instance, a well-structured business can respond more nimbly to regulatory changes or seize new market opportunities with fewer tax-related obstacles. Entrepreneurs often overlook the subtle interplay between short-term gains and long-term sustainability when making foundational tax decisions, but this foresight can be a competitive advantage.

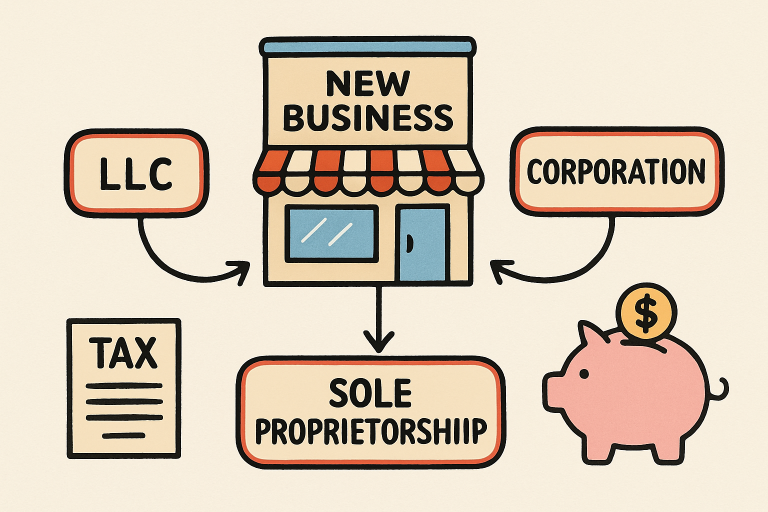

Choosing the Right Business Entity

The choice of business entity, such as a sole proprietorship, partnership, LLC, or corporation, affects taxation, liability, and operational flexibility. For instance, forming a C corporation can offer benefits like lower corporate tax rates and the ability to retain earnings within the company. However, it may also lead to double taxation when profits are distributed as dividends. Conversely, pass-through entities like S corporations and LLCs allow income to flow directly to owners, avoiding double taxation but potentially subjecting owners to higher individual tax rates.

Each business structure comes with distinct regulatory, accounting, and reporting requirements. For example, an LLC can offer flexible management while still providing liability protection to owners. It can also be taxed as a sole proprietorship, partnership, or corporation, giving founders additional strategic options. Partnerships, though offering simplicity and pass-through taxation, can create complexity around profit sharing and liability unless partnership agreements are drafted with care. Selecting the proper entity is not merely a tax consideration; it can also affect access to funding, eligibility for certain grants, and even branding.

Moreover, as a business grows, its needs may evolve, prompting a reassessment of its entity type. Many startups begin as LLCs or S corporations to take advantage of early-stage tax benefits and then convert to C corporations to attract investors and facilitate equity-based compensation.

Leveraging Tax Credits and Deductions

New businesses can benefit from various tax credits and deductions designed to encourage growth and innovation. For example, the Research and Development (R&D) tax credit allows companies to offset costs associated with developing new products or processes. Recent legislative changes have expanded these benefits, making them more accessible to startups and small businesses.

In addition to the R&D credit, businesses should consider credits for hiring employees from certain target groups, as well as deductions for energy efficiency upgrades, training expenses, and investments in capital assets. Continually monitoring newly enacted credits, such as those in legislative acts like the Inflation Reduction Act or state-specific innovation grants, can yield meaningful savings that free up cash flow for reinvestment.

Implementing Proactive Tax Planning

Proactive tax planning involves anticipating future tax liabilities and structuring operations to minimize them. This includes strategies such as income deferral, expense acceleration, and the use of tax-advantaged accounts. Engaging with a knowledgeable business lawyer can provide valuable insights into these strategies.

Forward-looking tax planning leverages historical data, forecasts, and scenario modeling to predict tax outcomes under different assumptions. For example, founders might time major equipment purchases or bonuses to align with the business’s cash flow needs or periods of higher income. Structured correctly, these actions can smooth out taxable income, minimize surprise tax bills, and ensure that growth initiatives remain adequately funded. Proactive planning also entails creating reserves for future tax payments to prevent tax obligations from disrupting cash flow.

Staying Compliant with Tax Regulations

Compliance with tax laws is crucial to avoid penalties and legal issues. This requires staying up to date on tax code changes and maintaining accurate financial records. The One Big Beautiful Bill Act (OBBBA) offers new tax-savings opportunities for many companies. Still, only 54% of finance leaders feel confident that their tax function understands how to reap its benefits.

Developing robust internal processes, utilizing reliable accounting software, and performing regular audits can help ensure ongoing compliance. These practices also foster transparency and facilitate smoother interactions with investors, lenders, or regulators. Compliance does not stop at paying taxes; it encompasses payroll administration, employment tax filings, and staying current on state and local requirements, which can vary significantly.

Adapting to Technological Changes

The integration of artificial intelligence (AI) and automation in tax preparation is transforming how businesses approach tax compliance and planning. Companies are evolving into strategic tax advisory firms, focusing on proactive planning rather than traditional tax filing.

New technologies help reduce errors and streamline data collection, analysis, and reporting tasks. Cloud-based accounting platforms can automate transaction entry, reconcile bank statements, and generate real-time tax projections. AI-powered platforms even provide predictive insights to help decision-makers optimize entity structure, employment taxes, or international transactions. Small and growing businesses, in particular, benefit from these tools, as they lower the barrier to sophisticated tax planning that was previously available only to large enterprises.

Considering International Tax Implications

For businesses operating globally, understanding international tax laws and treaties is essential. Proper structuring can prevent double taxation and take advantage of favorable tax jurisdictions. This requires careful planning and, often, consultation with experts in international tax law.

Global expansion introduces additional tax complexities, including transfer pricing, value-added tax (VAT) obligations, and country-specific reporting requirements. Establishing subsidiaries, creating holding companies, or forming strategic partnerships across different jurisdictions each has varying tax effects. Having a well-structured approach from the start ensures compliance with anti-avoidance rules and maximizes international profits. Global tax transparency initiatives, like the OECD’s BEPS (Base Erosion and Profit Shifting) framework, also make it more important than ever to document and justify cross-border tax strategies.

Conclusion

Smart tax structuring is a vital component of a new business’s strategy. By carefully selecting the appropriate business entity, leveraging available tax credits, engaging in proactive planning, and staying compliant with regulations, entrepreneurs can position their businesses for financial stability and growth. Consulting with experienced professionals, such as those at Freeman Lovell, can provide the guidance needed to navigate the complexities of tax structuring effectively.

Ultimately, a tailored approach, informed by experienced legal and financial partners, not only minimizes tax exposure but establishes the groundwork for sustainable, long-term growth. As tax laws evolve and new technologies shape the regulatory landscape, proactive, informed tax structuring will remain a cornerstone of successful business development. By taking a strategic, informed stance from launch, new ventures can thrive in an increasingly competitive market while reaping the enduring benefits of smooth tax compliance and maximized efficiency.