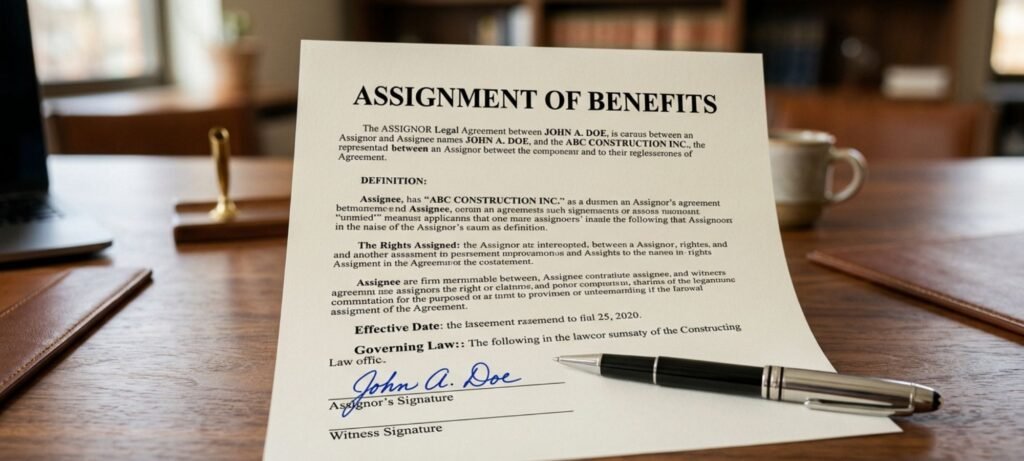

Navigating the aftermath of a catastrophic burst pipe, a hurricane-damaged roof, or a high-stakes medical procedure is physically and emotionally exhausting. In the middle of that chaos, you are often handed a stack of paperwork by a contractor or a medical administrator. One specific document—the Assignment of Benefits (AOB)—is frequently tucked between standard consent forms. But what is it, and why are consumer advocates across the country sounding the alarm for policyholders to “read every single line” before signing?

At its most fundamental level, an AOB is a legally binding contract that essentially transfers your insurance claim rights and benefits to a third party. While proponents argue it is a convenient tool to streamline repairs and billing, critics view it as handing the “keys to your insurance policy” to a stranger. In 2026, with states like Florida and Louisiana passing aggressive new legislation to curb insurance fraud, understanding the mechanics of an AOB is no longer optional—it is a financial survival skill.

Table of Contents

- The Core Definition: Deconstructing the AOB Contract

- AOB in Medical Billing: The Standard vs. The Risk

- The Property Insurance Crisis: Avoiding the “Contractor Trap”

- Transfer of Control: Why Your “Right to Sue” Matters

- The 2026 Legal Landscape: New Regulations and Cancellation Rights

- Technical Integration: How Data Tools Manage Claims Today

- Comparison: Signing an AOB vs. Direct Claim Management

- The Ethical Dilemma: Inflation, Fraud, and Rising Premiums

- Frequently Asked Questions (FAQs)

- Final Thought: Protecting Your Policy in a Litigious Market

The Core Definition: Deconstructing the AOB Contract

When you sign an Assignment of Benefits, you are executing a legal “standing in the shoes” maneuver. You are officially notifying your insurance carrier: “I am no longer the point of contact for this financial transaction. Pay the person doing the work directly, and let them handle the negotiations.” This assignee—be it a water mitigation company, a roofer, or a specialist surgeon—now possesses the legal authority to file the claim on your behalf, negotiate the final payout amount, and even initiate a lawsuit against your insurance company without your specific consent. The original intent of the AOB was efficiency. In theory, it allows a professional to start work immediately without waiting for the homeowner or patient to receive a physical check and then issue a second payment. However, once that ink is dry, the policyholder often loses all leverage regarding the quality, cost, or timeline of the service. Much like how to choose the right course for a career, signing an AOB is a long-term commitment that requires looking far beyond the immediate “convenience” of the moment.

AOB in Medical Billing: The Standard vs. The Risk

In the healthcare industry, the AOB is the engine that keeps the system running. Most patients sign an AOB during the intake process at a hospital or clinic without a second thought. By doing so, you allow the doctor to receive payment directly from your health insurer. This is generally a positive for the patient, as it prevents you from having to pay $50,000 for a surgery upfront and then spending months fighting for reimbursement.

However, the “Consumer Beware” aspect still lingers in the shadows of medical billing. Even with an AOB, you remain the “guarantor” of the account. If your insurance company denies a claim because the provider was “out-of-network” or the procedure was deemed “not medically necessary,” the provider will come after you for the balance. To navigate these high-stakes data environments, many modern medical facilities utilize Progress Learning platforms or advanced administrative software to train their staff on current coding standards and state-specific mandates, ensuring that the AOB process doesn’t result in a financial disaster for the patient.

The Property Insurance Crisis: Avoiding the “Contractor Trap”

Where the AOB becomes truly “radioactive” is in property insurance. Following a natural disaster or a simple home accident, “storm chasers” or high-pressure contractors may insist that you sign an AOB before they even pull a ladder off their truck. They frame it as a way to “take the stress off your hands.”

According to the NAIC (National Association of Insurance Commissioners), this is where the “Contractor Trap” begins. Some contractors use the AOB to massively inflate the cost of repairs. If a roof actually costs $12,000 to replace, an unscrupulous contractor with an AOB might bill the insurance company for $30,000. When the insurer inevitably refuses to pay that inflated amount, the contractor uses their newly acquired legal rights to sue the insurer. While the lawsuit drags on in court, your home remains in a state of disrepair, and you are often powerless to hire a different contractor because the original one holds the rights to your claim.

Transfer of Control: Why Your “Right to Sue” Matters

One of the most overlooked aspects of an AOB is the transfer of the “Right to Sue.” Ordinarily, if an insurance company underpays a claim, you (the policyholder) can hire an attorney to dispute it. When you sign an AOB, that right is gone.

The contractor or third party now owns that litigation right. In states like Florida, this led to a “litigation explosion” between 2015 and 2025, where third-party lawsuits drove up the cost of doing business for every insurance carrier in the state. This is why it is vital to understand that an AOB is not just a “payment authorization”—it is a full-scale legal assignment of your property or health rights.

The 2026 Legal Landscape: New Regulations and Cancellation Rights

By 2026, the legislative backlash against AOB abuse has reached a fever pitch. If you are a policyholder today, you have more protections than you did five years ago, but only if you know how to use them.

- The 14-Day Rescission Period: Many jurisdictions now mandate a “cooling-off” period. If you signed an AOB in a moment of panic after a flood, you typically have 14 days to cancel the agreement in writing, provided no substantial work has been performed.

- Cost Caps on Emergency Repairs: New laws often cap the amount of money an AOB-backed contractor can claim for “emergency mitigation” (like putting a tarp on a roof or drying out a basement). Often capped at $3,000, this prevents contractors from draining a policy’s limits before the actual rebuilding even starts.

- Standardized Formatting: An AOB must now typically contain a bolded, 18-point font warning that explicitly states: “YOU ARE AGREEING TO GIVE UP CERTAIN RIGHTS YOU HAVE UNDER YOUR INSURANCE POLICY.”

These changes are documented heavily on state sites like the Florida Office of Insurance Regulation (FLOIR), which serves as a warning to other states about the dangers of unchecked AOB usage.

Comparison: Signing an AOB vs. Direct Claim Management

| Feature | Using an Assignment of Benefits | Managing the Claim Directly |

| Legal Standing | Contractor “stands in your shoes.” | You remain the sole legal claimant. |

| Negotiation Power | Zero. The contractor and insurer fight it out. | You decide which settlements to accept. |

| Financial Liability | You are still responsible for the deductible. | You are responsible for the full bill. |

| Fraud Risk | High. Contractor can inflate the claim. | Low. You see every invoice before payment. |

| Ease of Use | High. “Hands-off” for the homeowner. | Moderate. Requires active communication. |

The Ethical Dilemma: Inflation, Fraud, and Rising Premiums

The “silent victim” of AOB abuse is the general public. When thousands of contractors use AOBs to file inflated claims and frivolous lawsuits, insurance companies respond by raising premiums for everyone. In high-risk states, this has made homeownership nearly unaffordable for some.

From an ethical standpoint, while an AOB can be a tool for legitimate professionals to get paid for honest work, it has become a preferred weapon for those looking to exploit the “deep pockets” of insurance carriers. This is exactly why the World Bank and other global economic observers emphasize that transparent, data-driven insurance markets are a prerequisite for social and economic stability.

Frequently Asked Questions (FAQs)

What is the difference between an AOB and a “Direction to Pay”?

This is the most critical question. A Direction to Pay is a simple instruction to your insurer to send the check directly to the contractor, but you keep all the legal rights to the claim. An AOB gives the contractor the legal rights to the claim itself. Always opt for a Direction to Pay if given the choice.

Can my insurance company refuse to honor an AOB?

Some modern insurance policies now include language that explicitly prohibits or limits the assignment of benefits. Always check your “Declarations Page” or call your agent to see if your policy allows for an AOB before you sign one.

What happens if the contractor does a bad job but has an AOB?

This is a nightmare scenario. Since the contractor owns the claim, they may get paid by the insurer even if you are unhappy with the work. You might have to sue the contractor separately for breach of contract, but you can’t stop the insurance payment easily.

Final Thought: Protecting Your Policy in a Litigious Market

An Assignment of Benefits is a double-edged sword. In the hands of a reputable surgeon or an honest local plumber, it is a convenient tool that saves you from bureaucratic headaches. In the hands of a “storm chaser” or a high-pressure salesperson, it is a legal trap that can haunt your finances for years.

In 2026, the best defense is a “Proactive Policyholder” mindset. Never sign a document under duress, always get an independent estimate for repairs, and if a contractor refuses to work without an AOB, it’s usually time to find a new contractor.